.png)

Model Implementations

Money Axioms

/

CAGR: The One Personal Finance Metric That Actually Matters

CAGR: The One Personal Finance Metric That Actually Matters

Personal finance is full of easy-to-remember rules. Start early. Save consistently. Invest for the long-term. These are the mantras repeated in books, blogs, and podcasts, always accompanied by charts showing a humble savings plan blossoming into millions if you just stick with it. But beneath all the slogans and colorful graphs, there is one metric that matters far more than any other: compound annual growth rate (CAGR).

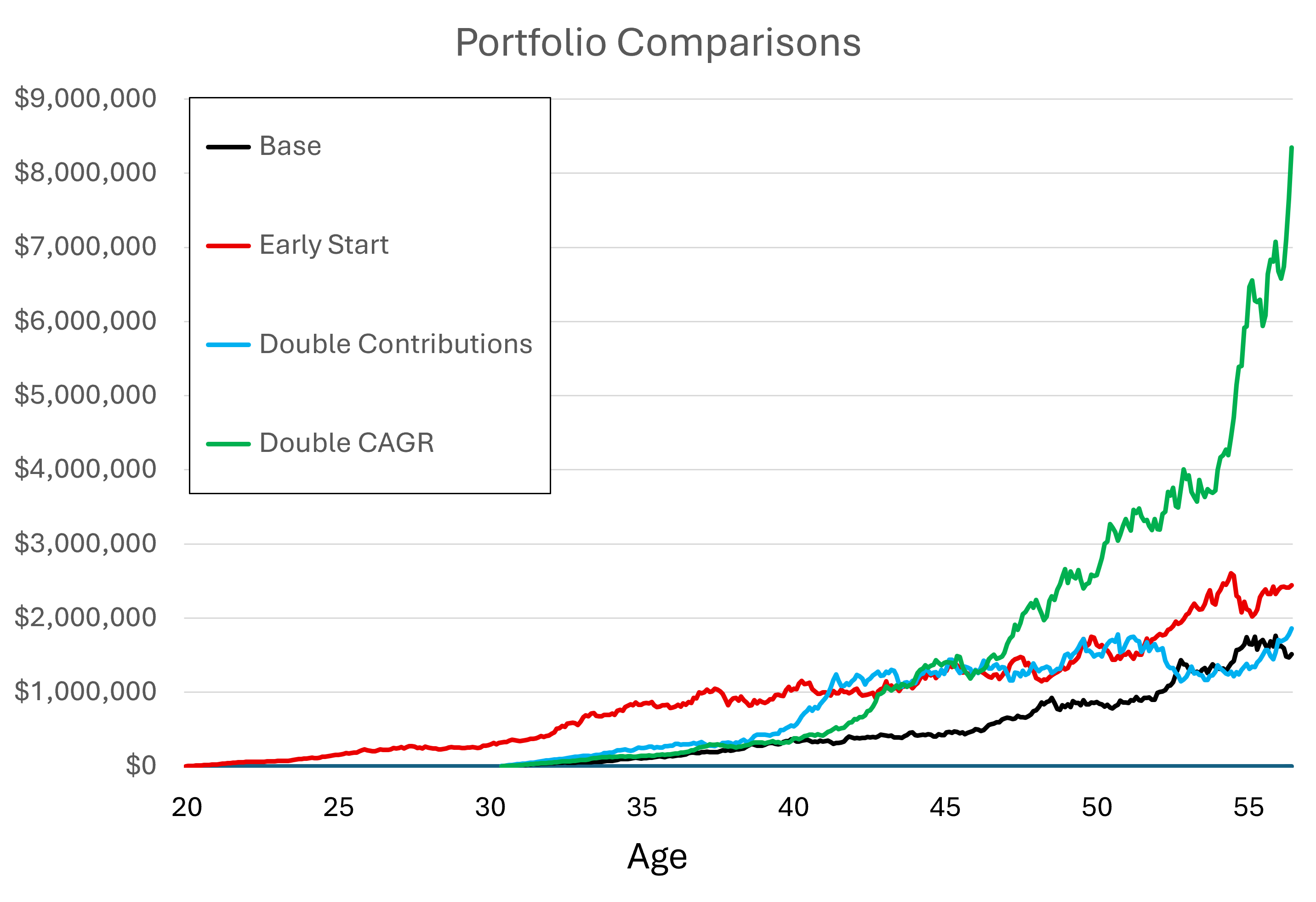

Every other lever of personal finance (e.g. when you start, how much you put in each month, how many decades you stay invested) has some effect on the outcome. But CAGR dictates the speed at which your portfolio compounds. A portfolio compounding at 4% doubles about every 18 years. At 8%, the same money doubles every 9 years. At 20%, less than 4 years. That single difference dwarfs the effects of starting a few years earlier or contributing a little extra.

In fact, this understates the significance of CAGR. The impact of increasing CAGR is actually two-fold. Not only does it result in faster growth as one approaches retirement, but if that growth is sustained throughout retirement, then it also increases the rate at which money can be spent before touching the principle. Your safe withdrawal rate is inherently chained to CAGR. If your CAGR is barely above inflation, drawing even 4% annually erodes your nest egg. If your CAGR is significantly higher, you can draw down comfortably without depleting your capital.

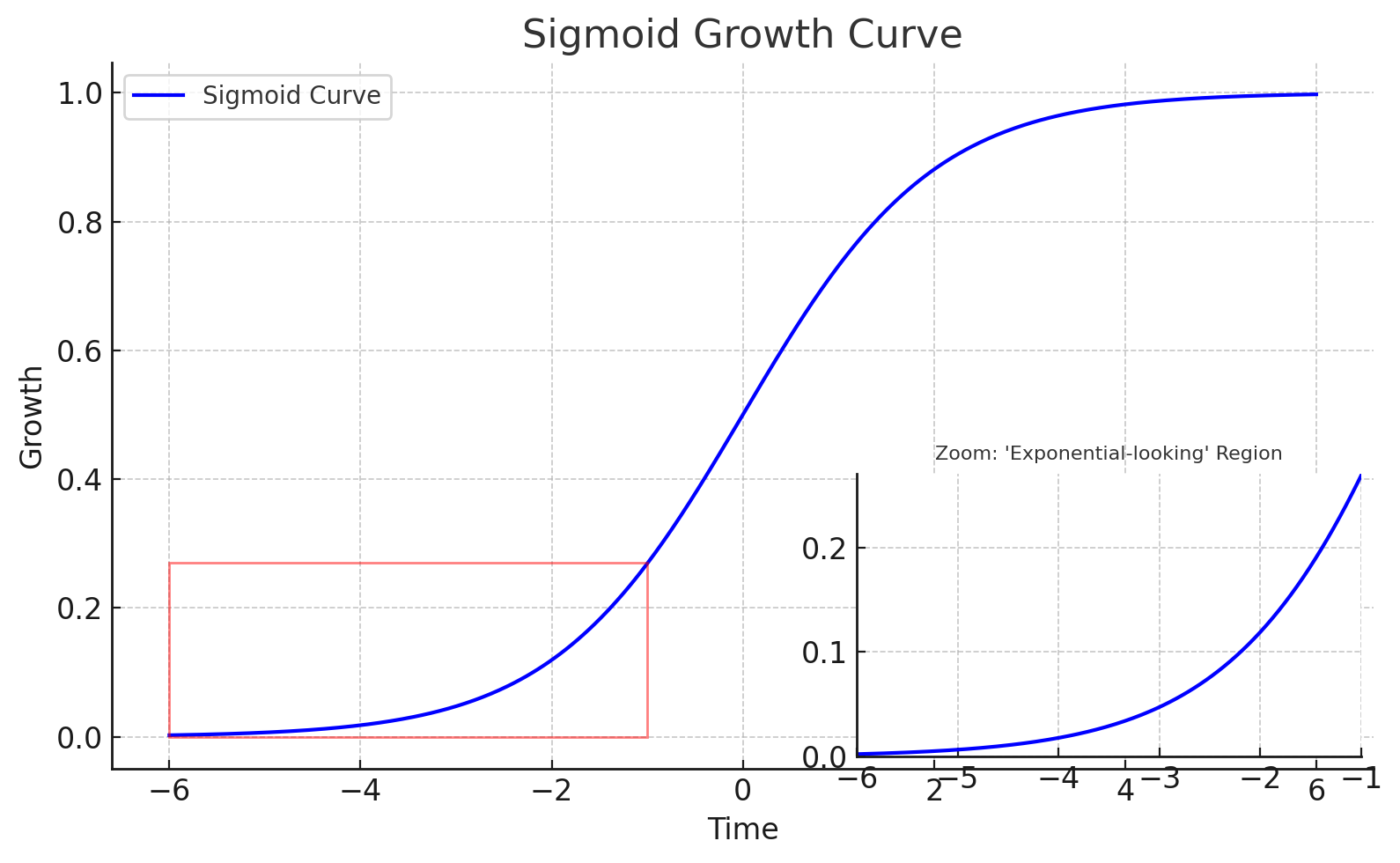

As an aside, it’s worth noticing how often personal finance gurus rely on the language of exponential growth. Their charts always look like neat, upward-curving hockey sticks, designed to make the audience dream of riches as long as they keep contributing. But the truth is that in nature, exponential growth almost never exists. What looks exponential is usually just the steep portion of a sigmoid curve that eventually flattens when the inflection point is passed. Bacteria populations, technology adoption, and the rise of empires all look to be exponential until they eventually don’t.

Moreover, even the earlier part of a sigmoid curve does not really describe the market. The fluctuations are extreme, and drawdowns can last for decades. The thesis is that enough time in the market will eventually capture the average historical growth rate, but that is a heavy assumption on which to rest one’s whole investing strategy.

But that aside only reinforces the main point: CAGR is the only number that truly matters. If your CAGR is low, you can save religiously for decades and still come up short. If your CAGR is high, even modest savings can balloon into something transformative. This is why it’s so striking that most finance advice barely touches the subject. For all their talk of expertise, gurus generally treat CAGR as a given, like the weather. Beyond your control, so not worth discussing.

Of course, it’s true that CAGR is not an easy variable to manipulate. So the advice of the gurus is to purchase broad index funds, with the promise that they will give you the market average, historically around 10%, or 7% after inflation. Active managers promise to beat that, though most never do. Alternatives such as real estate or private equity can sometimes raise CAGR, but they introduce risks and complexities, and it’s extremely hard to argue that those are truly passive investments. And so the conversation circles back to the comfortable advice. But then, what exactly are the gurus actually offering of value? If they ignore CAGR because they’re unable to influence it, then the work and the onus is entirely thrown back to the individual. Cut spending, save more, avoid salacious schemes, wait, be patient, and wait some more. So if every single guru will give the same advice, and that advice is to simply throw the ball back in your court, then what is the point of consulting them at all?

The result of all this is a strange silence around the one factor that actually decides financial outcomes. Your contributions and discipline matter, but they are secondary. CAGR is the engine. The most important question is not actually “Am I saving enough?” A thorough audit of one’s financial strategy would also ask “At what rate is my money compounding, and can I do anything sensible to improve that rate?” Until personal finance advice starts wrestling with that question, it will remain more about platitudes than about real growth.